A “TECHNICAL” CORRECTION—AND WHAT IS THAT, ANYWAY?

From its peak on January 29, the S&P 500 stock market index has fallen about 8%-fully half of those percentage points occurred on Monday. What started as an important (and perfectly normal) repricing in the bond markets, spilled into stocks triggering a cascade of technical selling.

“Technical selling” is a funny term. In short, it means that the selling has more to do with market structure than the fundamentals of an economy. This, in contrast to “fundamental selling”, which happens when the outlook for businesses has changed because of economic or corporate data.

Of course, most people don’t really care why selling happens, technical or not. No-one likes to see this much red. Discerning why a selloff has occurred is critical to determine how to proceed.

This technical selloff is being caused by a series of “triggers.” This began with a relatively mundane adjustment to interest rates which, taken alone, would be cause for little concern. However, they have compounded on one another creating this hard and fast selloff.

In this selloff, we have identified three major triggers. Let’s walk through these triggers one by one.

FIGURE 1.

1. DISCOUNT RATE.

“A bird in the hand is worth two in the bush.” (Anonymous proverb). In finance, this proverb about birds in bushes is quantified—that is, we recognize that a dollar today is worth more than a dollar tomorrow. In all stock pricing models, therefore, there is a discount rate used to “discount” the value of tomorrow’s dollar so it can be compared with today’s dollar.

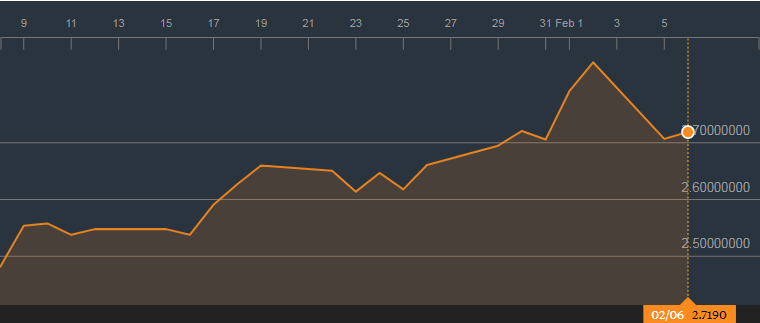

A common rate used to discount future dollars is the 10-year US Treasury yield. It has been easy to miss, but the 10-year US Treasury yield has increased significantly over the past few weeks, moving from 2.45% to 2.84% (see Figure 2). The reasons for this move are perfectly healthy: increased inflation expectations driven by consumer spending and higher wages (good) and the Federal Reserve raising interest rates because the economy is healthy (good), to name just two.

FIGURE 2.

Source: Bloomberg

However, this minor move in the discount rate can be shown to lower the value of future cash flows by about 3%. In other words, keeping all else equal, this move in the US Treasury yield over the past month could account for about 3% of the 8% selloff. Further, one could argue that the market has priced a new discount rate of 3.25%. The treasury yield has not hit that mark—it pulled lower after touching 2.84%--but markets are all about anticipation.

In Figure 1, I label this move with a big “1.” Again, this is a perfectly healthy move— and somewhat expected, though unconcerning

2. SMA 1.

Much has been made of the rise of automated trading algorithms—often called “algos” for short. There is, of course, no magic to an automated trading system. The machine will reflect the beliefs and trading style of its owner. One belief of market pricing (among many) held by various algo owners, is centered around the moving average of price. A Simple Moving Average (SMA) is among the most common form. The 20-day SMA is calculated by taking the average of the daily closing price over the past 20 trading days. This creates an indicator line on a chart (blue line in Figure 1). 3 According to the trading rules set by technicians, when prices move above (or below) these averages, the asset should be bought (or sold).

So, what started as a healthy discount-rate driven repricing (number “1” in Figure 1) managed to trigger a key technical level, the 20-day SMA, indicated by the number “2” in Figure 1. This level is heavily traded byalgos. As they all flashed “sell” together, markets began to move down very sharply.

This theory that algo trading has exacerbated the decline rests on two observations of market behavior from February 2. First, after the initial pullback, stocks traded mostly sideways for the week, until they crossed below this level. It was after prices crossed below this level that prices began to drop precipitously. Second, the number of shares trading hands increased sharply after prices crossed below this level. Indeed, volume increased about 50% in SPY and S&P 500 futures. Taken together with the suddenness of the drawdown, and it is a reasonable conclusion that algos were hard at work.

Though algos rapidly pushed prices down, it is important to remember that there was no significant news about the economy on that day—it was a technical selloff.

3. SMA 2.

No doubt, after a 6% swoon, investors went into the weekend wondering if they should move to the sidelines—it was Superbowl Sunday, after all. This, coupled with some momentum traders, would perfectly explain the further 1% downward open on Monday morning.

However, at 1:00 on Monday afternoon, the S&P 500 crossed another important technical level: the 50-day moving average. Because it represents a longer-term trend, this level is deemed to be more significant than the 20-day SMA discussed above, so again thealgos went to work. Again volume spiked (almost doubling, this time). Again, prices fell very rapidly. Again, this occurred only after this technical level was crossed. And again, there was no economic news significant enough to cause us to rethink our fundamental outlook.

THE NEXT TRIGGERS.

So what other levels are lurking to trigger the algos? Unfortunately, we are now not far from the 100-day moving average level of about 2630 for the S&P 500. As you can imagine, the 100-day level is even more significant than the previous two, so it would be no surprise to see sharp selling if this level is breeched. A hold above this level would bode well for near term price movement.

Further, because the upswing has been so long and strong, margin debt has likely grown a bit too large. This selloff will likely trigger some margin-based selling—i.e. investors selling because their loan increases the size of losses. In addition, there is some dislocation in the volatility-trading markets, forcing traders to scramble to cover their short volatility trades. These things, coupled with short covering, will likely exacerbate near-term price swings.

Finally, as mentioned above, markets may have priced a new US Treasury yield of 3.25%, but a swift move in that direction could lead to adjusted expectations in markets. In other words, a swift move in yields may generate some overreaction among investors. 4 In sum, all of these factors will likely lead to increased volatility in the near-term.

WHY I’M NOT WORRIED.

Sharp selloffs never feel good. They try our patience. What’s worse, they tempt us to do regrettable things. Ultimately, you are investing to achieve your goals, so my analysis always centers on determining whether your goals are at risk.

In short, the economic data points are good. Companies are making money and soundly beating expectations. The labor market is very good. People are being paid more. Indicators of manufacturing point to increased activity. International trade is healthy. Consumer confidence is sky high. While there is always risk on the table, we see little cause for concern with regard to the health of the overall economy. Therefore, we see this near-term bout of volatility as fleeting, though painful.

In these times of increased volatility and worry, it is important to evaluate three things:

- 1. Your tolerance for risk. Are you comfortable with the level of return and risk you are taking in your portfolio?

- 2. Your goals. Does a short-term selloff like this one affect your ability to achieve your goals?

- 3. Time horizon. Do you need your invested money soon, or are your goals longer-term in nature?

If these things haven’t changed, then it makes sense to continue with your long-term plan. As always, we are here to help you evaluate those questions, and to discuss how market behavior affects you. ■

--

All information provided herein is for informational purposes only and should not be relied upon to make an investment decision. This presentation is neither an offer to sell, nor a solicitation of any offer to buy any securities, investment products, or investment advisory service. The presentation is being furnished on a confidential basis to the recipient.

The information herein containsforward looking statements and projections representing the current assumptions and beliefs based on information available to Bright Wealth Management, LLC at time of publishing. This information included is believed to be reasonable, reliable and accurate, (however no representation is made with respect to the accuracy and completeness of such data) and is the most recent information available (unless otherwise noted). However, all the information herein, and such beliefs, statements and assumptions are subject to change without notice. All statements made involve risk, uncertainties and are assumptions. Investors may not put undue reliance on any of these statements. There is no guarantee that the market will move in any direction, as there is no way to predict with certainty future market behavior. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make an informed investment decision based on individual objectives and suitability. |